Hack your credit score: An easy way to a 800+ credit score

Imagine having a score so high you can get approved for anything and at a low-interest rate. Not only does a good credit score save you money, but it opens up more opportunities for you and just helps you relax, not stress and focus on what's important.

In my last credit hacking post, I mentioned I would give you some info that would really push your credit score past the 800 mark.

Now at this point, you probably pay all your credit cards on time. You have a 730+ credit score and always pay the full amount due on your cards every month. If this isn't the case check out my first post:

https://steemit.com/life/@veryrico/hack-your-credit-score-a-simple-method-for-huge-boost

The trick here is not just paying off the entire balance every month and never carrying a balance but to reflect on your credit report that you owe zero.

Now there is a huge difference between paying off your credit card every month and your credit report showing you have a zero balance.

Let me give you a couple of examples.

Let's say your bill is due on the 23rd, you pay the full balance and owe nothing but let's say your credit card reports to the credit bureaus on the 19th. Well, then every month, the credit card company reports you owe whatever the full balance of your card every month right before you pay it off.

Let's say it's backwards, let's say your due date is the 20th and your credit card company report the 25th. When you pay it on the 20th, you have a zero balance, but then you go buy a cheeseburger and some other things that equal $500. Now, the credit card company will report your new balance from the 20th - 25th of $500.

The trick here is to pay the card before the due date and right before they report.

For example, your bill is due the 20th, the credit card company reports on the 25th. You call the credit card company and get your due date changed to the 28th (just to have some leeway), and you pay your bill in full the 24th.

You're paying it four days earlier than the due date so you'll never be late, you pay right before they report to the credit bureaus so what gets reported is your zero balance. What it will say on your report is Bob spent 1k on his credit card but now owes zero.

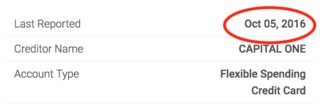

To find when your credit card company reports to the bureaus just pull up your report and look for "last reported on:"

Do this for three months in a row, and your score will skyrocket. Do this for a year, and you will be 810+ easy.

I look forward to hearing about your results and ask me any questions in the comments below.

I've always wondered how people got up to 850. It's a crazy game.

Included in Steemprentice Spotlight :)

Tweeted by SteemLand

Awesome, thanks man.

My credit score is finally up to 730 after two years of so-so payments. I finally paid the rest of my balance several months ago--and haven't used my card since. There hasn't been any change in my credit score. Is that because I'm not using my credit card?

Correct, if you use your cards and maintain a good credit history, your score will continue to go up.

Thanks for the information x 2

No prob, glad it is helpful.

Great credit score trick. Never thought about the concept of just asking for an extension. So simple, yet so brilliant:p

FYI - Credit Cards report to the credit bureaus the day your statement is cut, not the day the payment is due. So you want to pay down your credit card balance before you even get the statement. The act of doing this will not inherently increase your credit score unless your credit card balances are higher than 10% utilization the previous month. The ideal utilization ratio is 3-7% if you're shooting for an 800 score.

Attaining a perfect 850 credit score takes a lot of time and commitment. In fact, according to FICO, only 1.4% of the U.S. population falls in the "super-prime" category with a perfect 850 credit score. Personally, I think anything over 800 is good.

Agreed. Here is something you might find interesting.

Wells Fargo Credit Ratings

Excellent (760 and above)

You should generally be able to qualify for the best rates, depending on your debt and income levels and the amount of equity you have in any collateral.

Good (700 - 759)

You should typically be able to qualify for credit, depending on your debt and income levels and collateral value (but you may not get the best rates).

Fair (621 - 699)

You may have more difficulty obtaining credit, and will likely pay higher rates for it.

Poor (620 and below)

You may have difficulty obtaining unsecured credit.