How should we think about today's cryptocurrency prices?

Lately, I've been having conversation after conversation with friends and family about whether people should buy into cryptocurrency right now. There's such a wild sense in the crypto world of the money-making possibilities; peoples' eyes tend to bug out when you tell them that if you made less than 10x on your investment in 2017 that you're doing something violently wrong. Practically every single price chart for every single cryptocurrency looks like this:

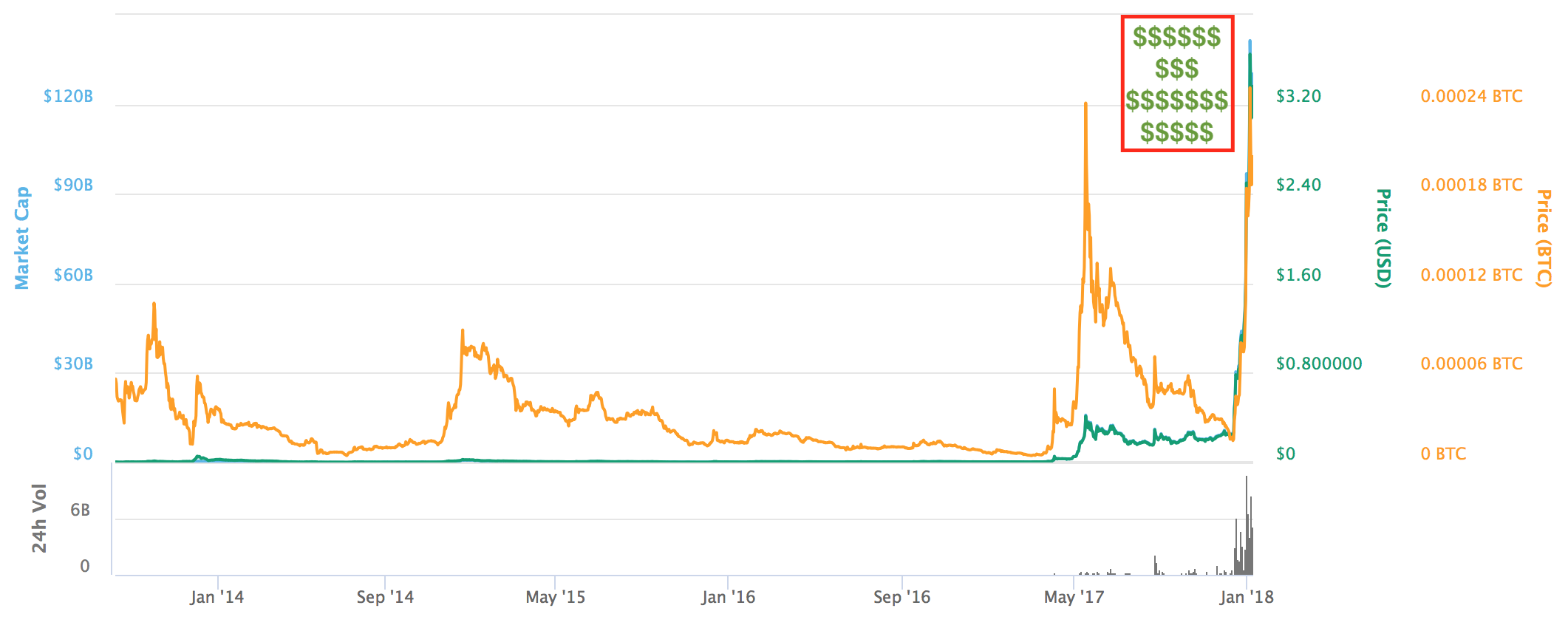

This is Ripple's all-time price chart from coinmarketcap.com

People see this and they feel like total dipwads for not buying Ripple (XRP) a year ago: in 12 months, XRP gave investors a 515x return! $2000 invested in XRP 12 months ago is now over $1 Million. So the natural question is something like this: "how much higher can it go?"

Everything that follows is my personal opinion, and not investment advice.

I first got into Bitcoin in November 2013 when the price of BTC was about $350. By the time I'd gotten myself verified with Coinbase and linked up a bank account, BTC was at $700 -- and it topped out just over $1000 before it started sliding back downwards for the next couple of years. In the meantime, I also got involved with Memorycoin (where my $100 investment was quickly worth less than $10) and Bitshares, and also picked up a few thousand Nxt and some other random coins. As prices were crashing, it all felt like an expensive hobby: lots of people talking about lots of interesting projects, but nobody really knew what cryptocurrency and blockchains were for. As a result, the air quickly escaped the bubble and prices fell to fairly low levels.

In 2014, quite a bit of money changed hands in cryptocurrency, but there wasn't anything like an economy.

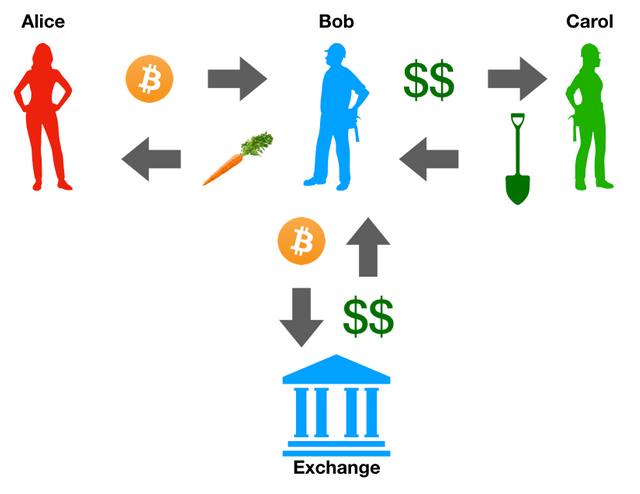

It seems to me that one of the reasons the 2013/2014 bubble popped so quickly was that there was no economy for cryptocurrencies. By "economy," I mean some kind of cycle of commerce: I trade bitcoin for carrots, my farmer trades bitcoin for fertilizer, the fertilizer guy trades bitcoin for machines, and the machine company pays me in bitcoin for engineering services. In 2014, there was no cycle. Almost any time you bought something with bitcoin, the person you sent the bitcoin to would simply sell it to pay their costs. If the farmer needs to buy fertilizer, but the fertilizer guy only takes cash, then the farmer needs to sell his bitcoin before he can engage in commerce.

The best we could do with cryptocurrencies in 2014. Carol doesn't accept bitcoin, so Bob has to trade his bitcoin for cash before he can trade with Carol. Not all that great, since when Bob sells his bitcoin to the exchange, it pushes down the price of bitcoin.

Is today really all that different?

Suppose that the fundamental problem in 2014 was that nobody knew what to do with their cryptocurrencies other than sell them. Is today really all that different? Is there something economically meaningful that you can do with your cryptocurrencies that you couldn't in 2014? Yes, there are some businesses which accept cryptocurrencies. It's a bigger scene now than it was in 2014, but at least in the United States there are some pretty severe barriers to commerce in Bitcoin.

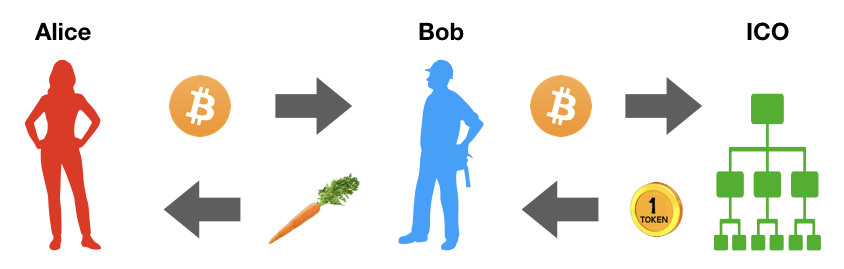

However, I'd argue that there is basically one major difference between 2014 and today: Today, there is unlimited demand for cryptocurrencies from ICOs. Not only is there unlimited demand for cryptocurrencies, but ICOs almost never even accept fiat currencies. (Yes, I know that ICOs existed in 2014 as well -- but not even remotely on the scale that they do now in 2017-2018. The big difference is Ethereum, which has been an extremely important enabling technology for fundraising.)

In 2018, Bob now has something to do with his bitcoins that does not involve immediately selling them: He can invest in the latest hot ICO!

How is this different from the 2014 picture? Now, there's something that anybody can do with their cryptocurrencies that delays their sale. Why is this important?

Every time you sell a Bitcoin, you directly push the price of Bitcoin down a tiny amount.

However, when you contribute a Bitcoin to an ICO, the price of Bitcoin essentially remains constant -- but now you have your magic ICO token that you bought, and you ascribe value to it because you traded something valuable for it. Get it?

On paper, by contributing a Bitcoin to the ICO, you just created a Bitcoin's worth of value out of thin air. The original bitcoin that you contributed still exists, but now you have these brand-new tokens that are also worth a Bitcoin. How do we know they're worth a Bitcoin? Because you just traded a Bitcoin for them.

Should that kind of value-printing magic make us nervous?

Maybe. It's always important in an asset bubble to ask "where is the value coming from?" In a perfect world, an ICO really does create literal value because it's putting funding in the hands of talented individuals who will be empowered to go employ their talents to build a powerful system.

However, in a world like today's where every ICO is giving investors immediate positive returns, it's likely that very many of those ICOs are not truly creating value; rather, they're just riding the wave of hype and leaching value out of the system. Unfortunately, I think it can be very difficult to tell which ICOs are "good" and which are "bad": the market might not immediately reflect that value is being leached out. This can lead us to a dangerous place where cryptocurrency prices are vastly higher than they truly deserve to be.

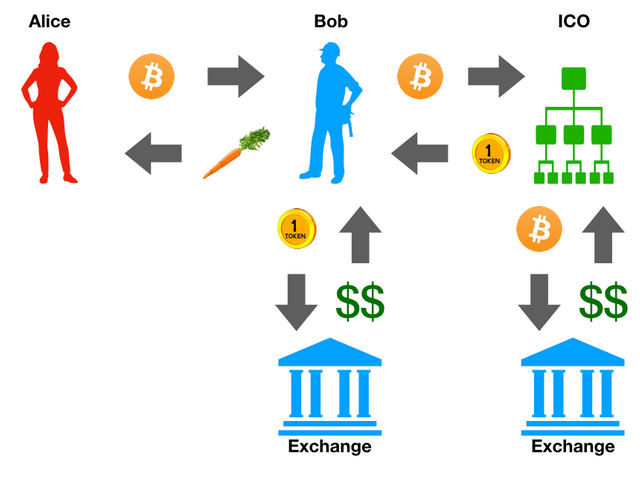

Furthermore, there still is no "cycle of value."

Recall that in 2014, Bob had to sell his bitcoin before he could engage in commerce. Today, that is still likely true for people who are raising money through ICOs. That is, the real picture probably looks like this:

Even though Bob didn't sell his bitcoin, the ICO will eventually have to as they pay employees, rent server space, etc. Also, remember that Bob needs money to buy tools -- so he'll have to sell his magic ICO token as well to pay Carol. Thus, the fact that there's demand for cryptocurrencies from ICOs doesn't mean that nobody will eventually sell the cryptocurrencies.

This is an idea that I'll continue to explore as I have time to write about it. Until then, I'd like to hear your thoughts on this question: "Are ICOs creating value out of thin air, and should we be worried about that?"

Finally... a good article. Thanks for that. I am following you now.

Just a thought: I believe the 'cycle' that you mention will only keep growing (or will only get more complete) in the future. You say that ICOs eventually need to sell the cryptos to pay their costs, and I agree that is true today. But as cryptos become more used (or mainstream), I believe some employees will eventually be willing to get paid in cryptos.

Think of an ICO in places with unstable economies like Zimbabwe (unlikely today, I know). Workers (and service prviders) will prefer to get paid in anything but their local currency.

Just like unstable governments have opted to use other currencies (e.g. USD) because theirs are simply too unstable, I think people and companies will eventually prefer cryptos over fiat currencies.

If I am a worker in Zimbabwe, I would rather receive my salary in frequent-flyer miles (I'm exagerating, but you get the point) than in fiat currency that can be controlled/frozen by my government or bank.

Voila - the economy closing the loop.

Yeah, I think that's all pretty much on the money. In the long term, I suspect that will happen more and more. But I'm guessing that it won't be a very smooth process; it'll happen with lots of jumps and starts and fortunes made and lost.

pocketsend:1001@antonio.mtw, thanks for the reply!

Successful Send of 1001

Sending Account: biophil

Receiving Account: antonio.mtw

New sending account balance: 828171

New receiving account balance: 1000

Fee: 1

Steem trxid: 2251a2da94ae485e05e6816051192f8b95bd1a6e

Thanks for using POCKET! I am running this confirmer code.

If there is no product or service that is actually used then the answer to both of your questions is yes. The real issue is...what will happen when the money stops flowing to the space? (I know it's a rethorical question).

Right. I tend to get fairly pessimistic when I go to answer that question.

A very good review, but I think you missed a crucial point about the crypto economy. To see that it does exist and actually works pretty well, we have to look how it changes the way we can look at money. For most of us, money is just a convenient alternative for barter, but a monetary system can also be looked at as a problem solving system. The thing is that with fiat money being so centralized and regulated, it was not worth while to look at it this way. In the cryptos reality, everything is moved by many small and cheap transactions ( by cheap I do not refer to the price of the coins but to the cost of setting up a transaction system, divided by the number of transactions ). In this situation, the potential of money as an optimization tool is unleashed. ICO’s are a good example. True. Most of them will not create any real value, but the cost of failure when money is recruited in an ICO, is much smaller than with a VC for example. This mean that more people, with a greater variety of initiatives are going to try, creating a better natural selection optimization process.

Very interesting perspective, and one which I need to spend more time thinking about. Do you have a mathematical background?

Mathematical background? I might. I have a lecture about that but it is in hebrew. I will try to write a post or a series of posts about this issue, altough I'm not sure I have the time for that right now...

You might? Oh. I think there might be a translation confusion. @biophil means, "have you studied math and/or have you worked in a math-related field?"

Ah okay 😐

So yes, I have a first degree in Mathematics, focused on what is now called, "applied mathematics".

Correct, that was what I was asking :)

The question of ICOs creating value out of thin air is complicated.

On the left hand, some ICOs promise new, futuristic, lightning fast algorithms that will compete with the giant bitcoin. These ICOs, which can reach massive heights, are taking value out of thin air. What have the contributed to the world? Is their product really any better than BTC? For the most part, these ICOs are nothing but smoke and mirrors to make its' creators millions.

On the right hand, however, we have companies like Siacoin, MusiCoin, Chartis, and Basic Attention Token which are providing actual products for consumers. These coins have intrinsic value, because people desire to use them. They are a consumer good in the base product.

BTC also has intrinsic value because it provided the block chain technology, and is the current exchange method for entrance into the crypto market.

Those are four projects I haven't taken the time to understand, but now I will. Thanks for the reference!

Another one I've been watching for a long time that has a real product launching soon is Lunyr.

Just looked into Lunyr, and Lord does this world need it to succeed!

Many ICOs are definitely cash grabs! Buzz words and good promotion still gets them a shitload of ETH/BTC despite very little fundamentals because investors speculate on big returns once the tokens hit the exchanges! As long as this works out for the investors, the ICO madness will go on and this will definitely continue to destabilize the market. To answer your question, yes many ICOs create value out of thin air as they will die out in the long run and we should definitely be worried about that!

Buzz words made me think of @kyriacos's fantastic satire piece: https://steemit.com/news/@kyriacos/buzzword-aims-to-revolutionize-cryptocurrency

This is one of those weird areas.

You can use value, to make more value, to make more value in a virtuous cycle.

The FED makes more inflation, to make more taxes, to make more theft, in a destructive cycle.

So, when you go and invest money into capital, then the whole world becomes better. With the flow of cryptos, capital is actually being formed. Capital that is providing service/value.

Or, basically, instead of having all of these houses mortgaged, and all these people saving in banks, if the people's savings where actually used on the mortgages, basically, all the mortgages get paid off. And, we are still left with all the houses. It is only by creating money out of thin air, that the houses can continually have a mortgage, that can never be paid off.

If we could get a person to pay off their house with cryptos, and then, that person helps the next, and then, that person... We truly would have all the houses paid off. And the banks would go nuts.

The banksters hate cryptos because it is giving capital to the wrong people.

Oh, and also: I agree. But at the moment, a great deal of that capital is probably just on paper -- that's the "thin air" part of my question. Is the cryptocurrency world generating enough economic activity to back up that paper capital?

Why would I pay off a 4% mortgage with capital I could invest at much higher returns in, say economic-activity-producing startup companies? I'm better off borrowing that money and having it invested in the economy. If I just close the loan, the money disappears and doesn't do anybody good any more.

That is, if you're interested in a little devil's advocate action.

Because, only in fractional reserve lending does buying a house create a sink. You pay four or five times for a house, and the money goes the bank to die. The houses never get paid off. Everyone just gets deeper in debt.

Mortgage - a french word meaning Death Note. Or, you will pay until you are dead.

With actual lending, all the houses get paid off, and because of that you get more and more people out of debt. First one, then another, then another. It is what happens when you do not send your hard earned labor to the banks to die.

Yes, I understand, if you have some ability to invest in these times, make better than 4%, you are basically paid to own a house. Both through the taxes, and through the banking system. But, the real number is the actual inflation which is about 12%, that is how much we are dying buy each year.

Inflation at 12%? This must be a case of using the same word to describe different things. I'll believe 12% when I see it, but I've certainly not had any personal experience of any such thing.

What's the tangible effect of your 12% inflation? (I'm assuming you mean something related to money supply, rather than something related to price levels.)

I like using shadow stats for numbers concerning the govern-cement.

And I personally use the burrito index or a similar, and much more tedious price tracking one (which I cannot remember the name)

Most of the created money is going into the stock market, so, the inflation is there... but most people consider it a good thing.

Hm. Last time the stock market collapsed, it was accompanied by a decrease in consumer price levels, which suggests that the high stock prices weren't being caused by anything quite as simple as money-printing; rather, the asset bubble was debt-related.

But your whole complaint is against fractional reserve anyway, so perhaps you agree.

So here's an interesting question, maybe we should start a top-level post to discuss it: how does a voluntaryist society prevent the emergence of fractional-reserve lending? It seems like fractional reserve banks are a very natural product of free markets.

Well, with block chain smart contracts, all those derivatives and debt swaps would have been triggered and all the money would have exchanged hands already. To the destruction of umpteen trillion dollars.

It is only because of obfuscation, and nobody pulling the trigger, that they remain.

If you do fractional reserve lending, at say 10%. You lend out the money 10 times. If one of those goes bad, you have lost all your money. So, in the realm of smart contracts, you go bust almost instantly.

If a bank / coin decided it was going to do fractional reserve, then the block chain using community would demand transparency on it, and you would very soon see the ponzi scheme of it.

Fair answer. For what it's worth, I bet you overestimate peoples' desire for transparency. Case in point: BitConnect and Tether. Both making billions of dollars in the blockchain-using community with business models that essentially cannot be made transparent. At least one of which almost certainly started as a ponzi scheme.

One thing that makes me nervous is the amount of stupid money being made. What I mean by this is when I ask someone why they bought a coin and their like because someone told me it's going to the moon. No idea about the coin, how it works, or why the price may increase just blind faith.

There sure does seem to be a lot of that sort of thing. Bitcoin has made so many accidental millionaires that there is a lot of uneducated money flying around.

"accidental millionaires"

:D

I wonder how much of a chain dependency to Bitcoin all other coins have. Could something like a Bitcoin crash pull all others down or could something like Steem survive the effect and continue to prove its true value?

Anything's possible, but I've suspected all along that a crash in bitcoin will bring everything down. Some might crash more gently than others, though.

That's exactly what's making me so hesitant to dab into the crypto currency market. If I'm brave enough, I could have jumped in a few months ago using what I've earned here as my seed money and ride the wave. I guess my returns could have far exceeded anything else.

Or I can try to understand the market better, do proper resesrch and seek those that does have some fundamentals behind it instead of just a gush of thin air.

Still working on the latter, but am aware I shouldn't drag my heels.

Crypto seems to capture a lot of the free talent that has been volunteering on the net for years.

There's a ton of value to capture, and we're going to see many more ICOs before the space is saturated.

pocketsend:101@protegeaa, yeah! Cryptocurrencies are providing all these cheap ways to monetize stuff, and I suppose that's part of what drives it.

Successful Send of 101

Sending Account: biophil

Receiving Account: protegeaa

New sending account balance: 829172

New receiving account balance: 1000101

Fee: 1

Steem trxid: 7c954bac59ffbcfb00baf93e57433056542d1cbe

Thanks for using POCKET! I am running this confirmer code.

pocketsend:52@biophil

Thanks for my first pocket tip! Giving some back to see if I know how to use the platform correctly.

Thanks! Your send didn't go through because you need a comma right after my account name:

pocketsend:52@biophil, then your message.pocketsend:53@biophil, thanks for the heads up!

Successful Send of 53

Sending Account: protegeaa

Receiving Account: biophil

New sending account balance: 1000048

New receiving account balance: 828224

Fee: 1

Steem trxid: 42dbc51dee855a3b5dcc3052a655efbf8bffa591

Thanks for using POCKET! I am small bot and right now I am running this code.

Successful Send of 53

Sending Account: protegeaa

Receiving Account: biophil

New sending account balance: 1000048

New receiving account balance: 828224

Fee: 1

Steem trxid: 42dbc51dee855a3b5dcc3052a655efbf8bffa591

Thanks for using POCKET! I am running this confirmer code.