Visa Begins Bribing Merchants To Stop Taking Cash

Authored by Yves Smith via Naked Capitalism blog,

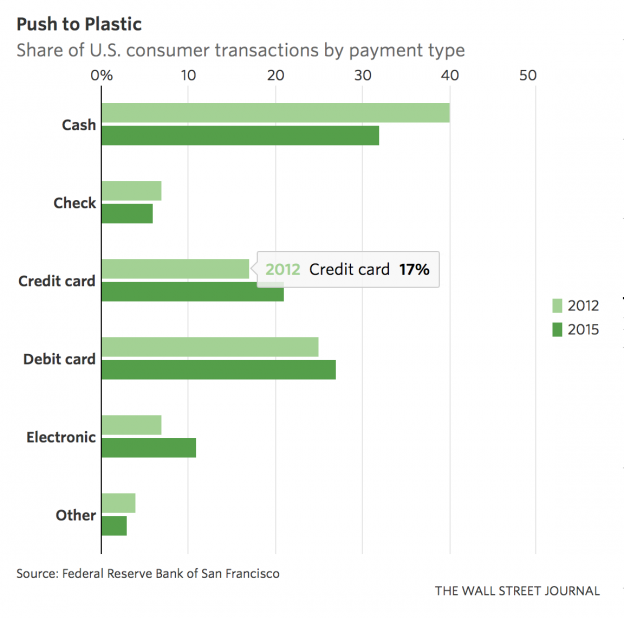

The war on cash is escalating. A big driver isn’t central banks who want to be able to inflict negative interest rates on savers, or Treasuries who see cash transactions as hiding revenues from their tax collectors, but the payment networks that want to kill cash (and checks!) as competitors to their oh so terrific (and fee-gouging) credit and debit cards.

However, one bit of good news is there doesn’t appear to be much enthusiasm on the buyer, as in merchant, end.

First, the overview from the Wall Street Journal:

Visa Inc. has a new offer for small merchants: take thousands of dollars from the card giant to upgrade their payment technology. In return, the businesses must stop accepting cash.

The company unveiled the initiative on Wednesday as part of a broader effort to steer Americans away from using old-fashioned paper money. Visa says it is planning to give $10,000 apiece to up to 50 restaurants and food vendors to pay for their technology and marketing costs, as long as the businesses pledge to start what Visa executive Jack Forestell calls a “journey to cashless.”

There are good reasons to think this initiative won’t get far.

Customer resistance. Food vendors, and in particular restaurants, are low margin businesses with fickle customers who have little to no loyalty. Why risk driving business away?

Aside from the fact that some customers prefer cash, a related issue is that using cards and smartphones often seem to be a tax on time. I really hate using chip cards. Mag cards were often faster than cash, since you swiped and could stuff the card back in your wallet while the transaction was being approved. Chip cards, by contrast, require you to keep the card in the machine while it is being approved, so one is very much aware of the wait. And when I’ve seen people using phones (often to buy small stuff like coffee, which really amazes me), I find that they are slower with it that they would probably be with cash, in that they seem to have to fumble with the phone to get the right app readied and then the payment doesn’t always go right through either.

And that’s before you get to the fact that ApplePay and other smartphone payments time stamp exactly when you paid, adding to the information the surveillance state is gathering about you. By contrast, even if you use a credit card at a store, Clive informs us that the card network typically retains only the date of transaction.

Higher merchant charges. I take credit and debit cards through PayPal, and also checks. And even though I am often slow to deposit checks because I find it hard to get to the bank, I’d still rather have checks despite the somewhat greater hassle because I save the 3% cut the card networks take. Visa makes the argument that handling cash has costs too, but they are the ones that have ginned up the numbers, and in my case, they don’t wash. As the Journal points out:

Indeed, many merchants prefer cash because they don’t have to share the revenue with card companies. Credit-card interchange fees, which networks like Visa set and that merchants pay to the banks that issue their cards, are on average around 2% of the transaction amount, according to the National Retail Federation, the largest trade group that represents merchants in the U.S.“The idea that merchants don’t want to accept cash is a myth,” said Mallory Duncan, senior vice president and general counsel at the National Retail Federation.

Negative impact on employees who get tips. As one of my tax attorney buddies drily remarks, “Some people have this odd idea that cash payments aren’t taxable.” Restaurant workers who have tips as the major source of their income almost assuredly prefer getting them in cash, rather than facing the delay of having their employer receive them through the payment network which creates delay as well as the not-trivial odds that the boss might cheat them either informally or declare that he’s entitled to a processing cut. And that’s before getting to the fact that restaurant pay levels probably pre-suppose a fair bit of tax evasion, so the business owner might risk losing his better employees to competitors who hadn’t gone the no-cash route.

Enforcement. How is Visa going to police establishments that say they aren’t going to take cash? Will Visa have spies? Will Visa have audit rights?

Risk of legal challenge. As a surprisingly large number of Wall Street Journal readers pointed out, cash is a legally sanctioned means of payment. For instance:

Richard Tavis

Merchants who will no longer accept cash won’t get my business, period. Call me a Luddite, but U.S. currency pretty clearly states that “THIS NOTE IS LEGAL TENDER FOR ALL DEBTS, PUBLIC AND PRIVATE”. It seems to me this will go to court eventually. Merchants must accept notes issued by the Fed. Sorry, that’s the way it is.

Richard Tauchar

That’s my take as well.

And, as someone else mentioned, what happens if you refuse to pay with a Visa, or don’t have one, after having completed the meal? Will they take cash then, or is the meal free?So I’d be surprised if Visa had a legal leg to stand on, when trying to make these deals.

The Treasury does support the position that private business can refuse to take cash as payment for goods and services, as opposed to settlement of debts.

However, as writers following David Graeber’s Debt: The First 5000 Years, like to point out, we incur and settle debts all the time. And a bar tab or restaurant bill is a debt. The vendor provides the service<strong> without being paid, then expects you to settle the debt you incurred.

Thus the market segment Visa is targeting for this move (the Wall Street Journal headline says, Visa Takes War on Cash to Restaurants) would seem to be one where Visa is on a particularly weak legal footing. I can easily see someone with a penchant for mixing things up go to a restaurant, either not have a card or bring a card he knows will be declined (just to look like he didn’t intend to stage a stunt) and then video putting down more than enough cash to settle the bill and leave. The merchant will have no legal out. He’s been paid. And at least in any decent-sized city, no way will the cops intervene. They’ll regard this as a private dispute not worth their time. If the restaurant staff try to restrain the exiting customer, they could wind up with a very costly suit on their hands.

Taking cash may be the real point of the merchant. A savvy New York City colleague regularly points out how many New York City businesses, like pizzerias and cheap jewelry stories that never seem busy, or nail salons that have economics that don’t seem to make sense, are probably partly if not mainly in the money laundering business.

Source : ZeroHedge

Disclaimer : This is not the real Tyler Durden. I read ZeroHedge every day and share the best articles about cryptocurrencies, politics and economy on Steem. You can head over to ZeroHedge's website for more content.

Here's where it starts. And, whoever does take the money will also likely get a ton of free publicity beyond this.

I'm typically amazed how long cash will last in my wallet. Since I get money back from my credit companies - 5% on gas, 3% on groceries & restaurants, 1.5% on everything else - I typically would rather charge it and keep my cash for later.

Ultimately, though, I look forward to paying with my cryptowallets.

Fees will ALWAYS be passed onto the consumer. No matter what a merchant advertise the price as, any fees they are copping are always incorporated.

This is a real war people. The deep state is trying multiple methods to monitor cash movements and digitalise hard cash into fiat. Stay in gold and crypto my friends. They are even going as far as monitoring fiat with nanotechnology.

https://steemit.com/steemit/@banglasteve/nanotechnology-to-track-cash-movements

Scary times. But maybe its whats needed to make cryptos more popular.

Hi @zer0hedge thanks for your post. Yes last year the EU parliament has voted a law to end up cash in Europe within the next three years and now they start to promote the R.F.I.D. for all European citizen. Anyway since we enter Europe it is worth than communism. I really hope we get rid of this shit of EU. My home country (France ) had voted in 2005 no to integrate EU but our politicians have said we are not educated enough to understand so they bring us into the EU. I am so happy to live 10 000 Km away from this nonsense. Love and Happiness to all of you

None of that is true.

Up to you

The things we normal people never even think about are the things that large businesses and corporations are masterminding

Fee's aside, it must be easier for a merchant to take cards over cash. No risk of loss (robbery or employee theft), easier processing, no bank runs, issues with change etc etc. Its the technology and fees that must be the issue! aside from the laundering angle that is.

Interesting, I think they are doing everything to get us to digital, and cash I'm pretty sure is on its way out sooner then we think.

Thanks for the post.

I'm gonna Re-STEEM

terrible for merchants!, even though i love using my cards as a customer

When there's no cash in hand then what will folks do if/when something crashes (like the grid and the economy)? Please, please....we need cash, we need coins (silver and gold), we need to barter and trade, we need to make our own local currencies.

I use plastic and cash. I even still write checks for bills. (I also don't own a smart phone but an older model flip phone.) I just don't think it is safe or healthy to ONLY use credit/debit cards. This is a recipe (yet another) for disaster.